Arkansas Mortgage Calculator

Your Home Loan Estimate

Your Estimated Payment

Boost your score to 760+

Save $140/month or $50,820 over 30 years

Buying a house in Arkansas doesn’t require a perfect credit score, but it does require a clear understanding of what lenders actually look for. Many people assume they need a score of 800 or higher to get approved - that’s not true. In fact, you can buy a home in Arkansas with a credit score as low as 580, depending on the loan type. The real question isn’t just about the number - it’s about how that number affects your options, your monthly payments, and your long-term financial health.

Minimum Credit Scores for Different Loan Types in Arkansas

Not all mortgages are the same. The credit score you need depends on the kind of loan you apply for. Here’s what most Arkansas homebuyers actually use:

- FHA loans: Require a minimum score of 580 for a 3.5% down payment. If your score is between 500 and 579, you can still qualify - but you’ll need to put down at least 10%. FHA loans are popular in Arkansas because they’re forgiving for first-time buyers and allow gift funds for down payments.

- Conventional loans: Most lenders in Arkansas want a score of 620 or higher. Some private lenders may go as low as 600, but those are rare. These loans usually require a 3% to 5% down payment and have stricter income and debt rules.

- VA loans: Available to veterans, active-duty service members, and eligible spouses. There’s no official minimum score set by the VA, but most Arkansas lenders require at least 620. These loans require zero down payment and no private mortgage insurance.

- USDA loans: Designed for rural and suburban homebuyers in eligible Arkansas counties. The typical minimum score is 640, though some lenders may accept 620. These loans also offer zero down payment and low interest rates.

Most Arkansas homebuyers in 2026 are using FHA or conventional loans. VA and USDA loans are less common but still viable - especially in smaller towns like Little Rock, Fayetteville, or Pine Bluff where housing costs are lower than in big cities.

How Your Credit Score Affects Your Interest Rate

A credit score of 620 might get you approved, but it won’t get you the best rate. In Arkansas, lenders use your score to decide how risky you are. Here’s what that looks like in real dollars:

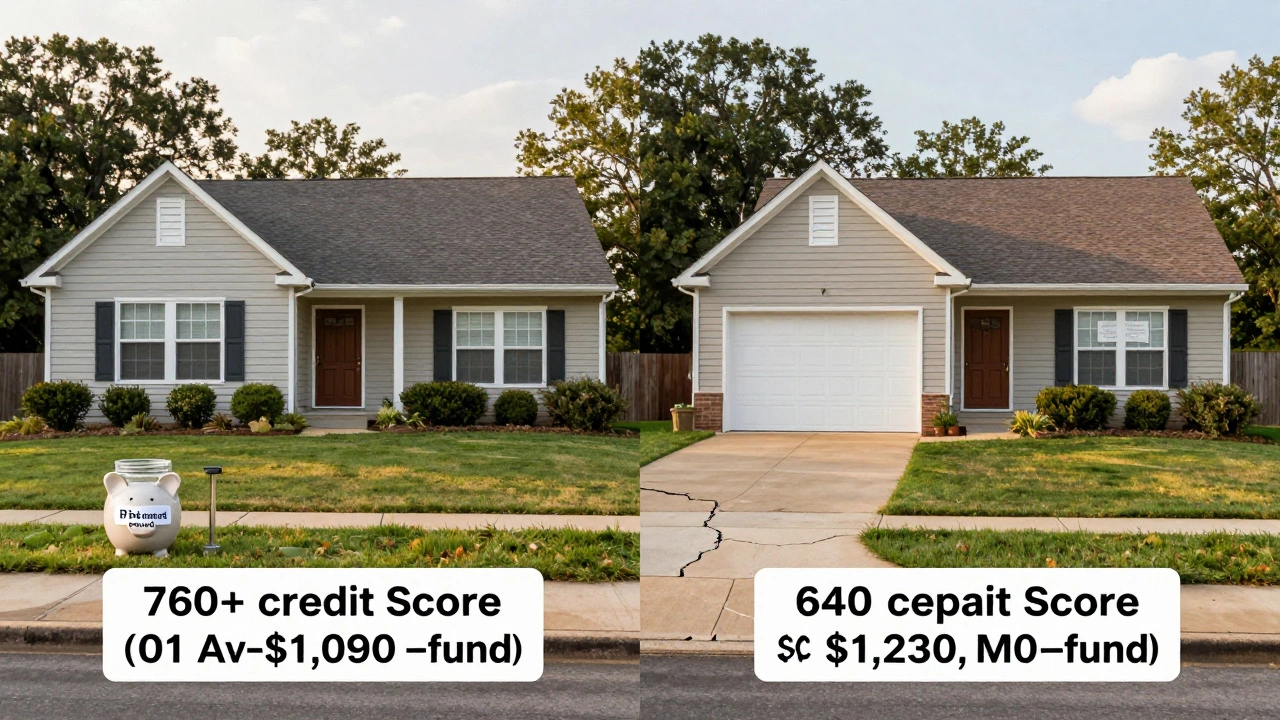

Let’s say you’re buying a $200,000 home with a 10% down payment. That means you’re borrowing $180,000. With a credit score of 760+, you might lock in a 6.1% interest rate. Your monthly payment would be about $1,090.

But if your score is 640, you could end up with a 7.3% rate. That same $180,000 loan jumps to $1,230 a month. That’s $140 extra every month - over $1,600 a year. Over 30 years, that’s more than $50,000 in extra interest.

That’s why improving your score by even 30 points can save you tens of thousands. You don’t need to be perfect. Just being in the 700-749 range can drop your rate by half a percent or more.

What Else Lenders Look At in Arkansas

Your credit score isn’t the whole story. Arkansas lenders also check:

- Debt-to-income ratio (DTI): Your monthly debt payments (car loans, credit cards, student loans) divided by your gross monthly income. Most lenders want this under 43%. Some FHA lenders allow up to 50% if you have strong income or savings.

- Down payment: The more you put down, the more forgiving lenders are. A 20% down payment can help you qualify even with a lower score.

- Employment history: Two years of steady work is standard. Self-employed buyers need two years of tax returns and often higher credit scores.

- Recent credit mistakes: A bankruptcy from five years ago? That’s usually fine. A missed payment last month? That’s a red flag.

One Arkansas lender in Bentonville told me last year that 62% of applicants with scores under 650 were denied - not because of the score alone, but because they had multiple recent late payments or high credit card balances. Fix those first, and your score becomes a much smaller hurdle.

How to Raise Your Score Quickly in Arkansas

If you’re planning to buy in the next 6-12 months, here’s what actually works in Arkansas:

- Pay down credit card balances: Aim to use less than 30% of your available credit. Paying off a card that’s at 90% usage can boost your score by 40-60 points in one billing cycle.

- Check your credit report: One in five Arkansans has an error on their report. Dispute anything wrong - late payments that weren’t late, accounts you didn’t open. You can get free reports at AnnualCreditReport.com.

- Don’t open new credit: Applying for a new credit card or car loan right before you apply for a mortgage can drop your score. Wait until after closing.

- Ask for a credit limit increase: If you’ve been paying on time for a year, call your credit card issuer. A higher limit lowers your utilization ratio - and your score rises.

One woman in North Little Rock raised her score from 612 to 708 in five months by doing just those four things. She bought her first home in January 2026 with a 3.5% FHA loan.

Arkansas-Specific Programs That Help

The Arkansas Development Finance Authority (ADFA) runs programs that make homeownership easier:

- First-Time Homebuyer Program: Offers down payment assistance up to $10,000 for qualifying buyers. You don’t need perfect credit - a score of 620 is enough.

- Homeownership Counseling: Free classes offered in 12 Arkansas counties. They help you understand credit, budgeting, and the loan process. Many participants walk away with a 50-point score boost.

- Homebuyer Education Grants: Some counties offer grants to cover closing costs if you complete a course.

You can find these programs through your local housing authority or by visiting adfa.org. These aren’t just for low-income buyers - even middle-income families in Fort Smith or Rogers qualify.

What to Avoid When Buying a House in Arkansas

Here are three common mistakes that derail Arkansas homebuyers:

- Buying before fixing credit: Don’t rush into a home if your score is below 580. You’ll pay more in interest, get stuck with higher insurance, and have fewer options.

- Using a real estate agent who doesn’t know local programs: Some agents push conventional loans even when FHA or USDA would save you money. Find one who works with ADFA or local housing nonprofits.

- Ignoring closing costs: In Arkansas, closing costs average 2%-5% of the loan. If you’re buying a $180,000 home, that’s $3,600-$9,000. Some programs let you roll this into the loan, but not all lenders allow it.

One man in Jonesboro tried to buy a house with a 590 score and no savings. He was approved - but his monthly payment was $1,400. He couldn’t afford repairs, insurance, or groceries. He lost the house six months later. Don’t be that person.

Final Thoughts

You don’t need a 750 credit score to buy a house in Arkansas. You need a plan. Start by checking your score. Then, focus on lowering your debt, fixing errors, and saving for a down payment. Use the state’s free resources. Talk to a housing counselor. And don’t let a low number stop you - just let it guide you.

There’s no magic number. But there is a path. And in Arkansas, that path is clearer than most people think.

What is the minimum credit score to buy a house in Arkansas?

The minimum credit score to buy a house in Arkansas is 500 for FHA loans, but you’d need a 10% down payment. For a 3.5% down payment, you need at least 580. Most lenders prefer 620 or higher for conventional loans. VA and USDA loans typically require 620-640.

Can I buy a house in Arkansas with a 600 credit score?

Yes, you can buy a house in Arkansas with a 600 credit score. You’ll likely need an FHA loan and a down payment of at least 3.5%. You may also face higher interest rates and stricter income requirements. Improving your score to 640 or higher can save you thousands over the life of the loan.

Does Arkansas have first-time homebuyer programs?

Yes. The Arkansas Development Finance Authority (ADFA) offers down payment assistance up to $10,000, free homebuyer education, and closing cost grants. These programs are available to buyers with credit scores as low as 620 and are not limited to low-income households.

How long does it take to improve a credit score enough to buy a house?

You can see noticeable improvements in 3-6 months by paying down credit card debt, disputing errors, and avoiding new credit applications. Some people raise their score by 50-100 points in under four months. Consistent on-time payments and low credit utilization are the most effective tools.

Do I need perfect credit to get approved for a mortgage in Arkansas?

No. Perfect credit is not required. Many Arkansans buy homes with scores between 620 and 680. What matters more is your debt-to-income ratio, down payment size, and employment stability. Lenders care more about your overall financial picture than a single number.